FUND OBJECTIVE: The Fund aims to achieve for its participants income and liquidity by investing in a portfolio of short-term dollar-denominated fixed income securities and money market instruments with a maximum weighted average duration of one year.

| FUND SUMMARY of Metrobank MetroDollar Money Market Fund |

|||

| • NAV | : | USD 13.12 Million | |

| • NAVPU | : | 1.213691 | |

| • WtdAve YTM | : | 1.962% p.a. | |

| • Wtd Ave Term | : | 1.05 years | |

| • WtdAve Duration | : | 0.89 years | |

PRODUCT FEATURES |

|||

| • Base Currency | : USD | ||

| • Min. Initial Participation | : USD 2,000 | ||

| • Min. Add’l. Participation | : USD 1,000 | ||

| • Investment Horizon | : Six months | ||

| • Min. Holding Period | : 45 calendar days | ||

| • Early Redemption Charge | : 50% of income earned from the redeemed amount | ||

| • Trust Fee | : 1.0% p.a. based on NAV | ||

| • Custodian Fee | : 0.0175% p.a. | ||

| • Applicable Tax | : 7.5% Final Tax | ||

| • Valuation | : Marked-to-Market | ||

| • Dealing Day | : Daily up to 12:00nn | ||

| • Redemption Settlement | : Next Banking Day From Date of Redemption | ||

| • Fund Manager | : Metrobank-Trust Banking | ||

| • Custodian | : Citi bank N.A. | ||

| • Launch Date | : March 1, 2007 | ||

OTHER DISCLOSURES

1. Prospective investment outlets shall be limited to those described in the Declaration of Trust of the Fund.

METROBANK METRODOLLAR MONEY MARKET FUND PERFORMANCE as of 2/28/2011

| Period | Fund | Benchmark |

| Past 30 days | 0.22% | 0.12% |

| Past 90 days | 0.31% | 0.13% |

| YTD | 0.26% | 0.13% |

| YOY | 2.39% | 0.14% |

| Past 3 Years | 14.21 9% | 0.41 5% |

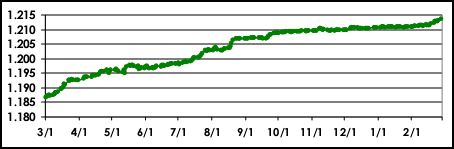

NAVPU TREND, Year-to-Year

METROBANK METRODOLLAR MONEY MARKET FUND TOP 10 HOLDINGS

| Security | % |

| TD - Other Bank | 7.90% |

| $ROP 01/21 4 | 7.22% |

| TD -Other Bank | 6.18% |

| TD - Other Bank | 4.98% |

| TD - Other Bank | 4.60% |

| TD - Other Bank | 4.58% |

| $CBSM 1071813 | 4.57% |

| TD - Other Bank | 3.81% |

| TD - Other Bank | 3.74% |

| TD - Other Bank | 3.33% |

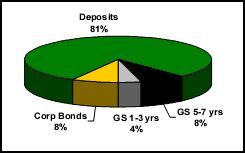

METROBANK METRODOLLAR MONEY MARKET FUND COMPOSITION

FUND MANAGER’S REPORT

- https://www.affordablecebu.com/

USD Bonds/ROP

By Tony C. Pineda

Social discontent continues to grip the Middle East and the North African regions. After political anxieties engulfed Tunisia, Egypt, and Bahrain, Libya now holds world markets hostage as strongman Gadhafi clings to power amidst public clamor to step down.

US Treasuries provided a safe haven for investors as risk was once again taken off the table. Despite positive economic data in the US, Treasuries shaved off yields as flight to quality trades drove bond prices up. The 10-year yield peaked at 3.74%-3.78% in the first half of February at the height of inflation cum economic recovery episode in the US as players positioned ahead of the curve. By the end of the month, the 1 0-yr yield settled at 3.43% showing a month-on-month (m-o-m) yield drop of close to 6 basis points (bps). The biggest gainer was the 5-yr tenor which shed almost 20 bps m-o-m.

The stubbornness of Gadhafi poses a grave threat to global oil price stability. Despite a ranking of 13th in terms of global oil production, Libya is an abundant source of the light sweet blend, a favored variant for transportation fuel. The possible supply shock threat has driven up the price of crude oil by more than 5% for February (at $96.97/barrel) or more than 6.5% since December 2010. Some central banks in emerging markets have in fact held off aggressive monetary tightening to cut some slack as the oil price pressure shows no sign of easing.

The risk of higher oil prices is slowly finding its way into the CPI inflation basket. Ironically, global equity markets continue to enjoy buoyant sentiment and Asian credit markets are also relatively strong. The higher price of oil somehow brought back into the limelight some oil producing emerging market economies such as Russia and Kazahkstan which stand to benefit from higher oil prices. Sovereign bond prices of other fundamentally sound and promising economies are holding despite a downward bias provided by the oil wildcard..

Selected ROPs in the intermediate and long end bonds have already shown price gains of as much as 0.66%, something which we have not seen for the first two months of the year.

OUTLOOK and STRATEGY

Despite signs of hope for ROPs and other emerging market debt, this is definitely not the proper time to be aggressive for bonds. Current inflationary concerns exacerbated by the possibility of an oil supply shock dictate us to adopt a defensive stance.

The current threat to core inflation and a seemingly stabilizing unemployment rate in the US could cause the Fed to reassess their accommodative stance in the upcoming March 15 meeting. Although on previous occasions, Fed Chairman Bernanke still favors the continuance of stimulus efforts and discounts the likelihood of a prolonged effect the current spike in oil prices would have on inflation.

Participation in the Fund is NOT a bank deposit or an obligation of, or guaranteed, nor issued, nor insured by Metropolitan Bank & Trust Company or its affiliates or subsidiaries and therefore are not insured or governed by the Philippine Deposit Insurance Corporation (PDIC). Any income and loss arising from market fluctuations and price volatility of the securities held by the fund, even if invested in government securities, is for the account of the investor. As such the fund is not capital protected and may not be suitable for clients seeking preservation of capital. Historical performance when presented is purely for reference purposes and not a guarantee of similar future results. The Declaration of Trust of the Fund is available at the principal office of the Trustee upon request.

Source: metrobank.com.ph

By Tony C. Pineda

Social discontent continues to grip the Middle East and the North African regions. After political anxieties engulfed Tunisia, Egypt, and Bahrain, Libya now holds world markets hostage as strongman Gadhafi clings to power amidst public clamor to step down.

US Treasuries provided a safe haven for investors as risk was once again taken off the table. Despite positive economic data in the US, Treasuries shaved off yields as flight to quality trades drove bond prices up. The 10-year yield peaked at 3.74%-3.78% in the first half of February at the height of inflation cum economic recovery episode in the US as players positioned ahead of the curve. By the end of the month, the 1 0-yr yield settled at 3.43% showing a month-on-month (m-o-m) yield drop of close to 6 basis points (bps). The biggest gainer was the 5-yr tenor which shed almost 20 bps m-o-m.

The stubbornness of Gadhafi poses a grave threat to global oil price stability. Despite a ranking of 13th in terms of global oil production, Libya is an abundant source of the light sweet blend, a favored variant for transportation fuel. The possible supply shock threat has driven up the price of crude oil by more than 5% for February (at $96.97/barrel) or more than 6.5% since December 2010. Some central banks in emerging markets have in fact held off aggressive monetary tightening to cut some slack as the oil price pressure shows no sign of easing.

The risk of higher oil prices is slowly finding its way into the CPI inflation basket. Ironically, global equity markets continue to enjoy buoyant sentiment and Asian credit markets are also relatively strong. The higher price of oil somehow brought back into the limelight some oil producing emerging market economies such as Russia and Kazahkstan which stand to benefit from higher oil prices. Sovereign bond prices of other fundamentally sound and promising economies are holding despite a downward bias provided by the oil wildcard..

Selected ROPs in the intermediate and long end bonds have already shown price gains of as much as 0.66%, something which we have not seen for the first two months of the year.

OUTLOOK and STRATEGY

Despite signs of hope for ROPs and other emerging market debt, this is definitely not the proper time to be aggressive for bonds. Current inflationary concerns exacerbated by the possibility of an oil supply shock dictate us to adopt a defensive stance.

The current threat to core inflation and a seemingly stabilizing unemployment rate in the US could cause the Fed to reassess their accommodative stance in the upcoming March 15 meeting. Although on previous occasions, Fed Chairman Bernanke still favors the continuance of stimulus efforts and discounts the likelihood of a prolonged effect the current spike in oil prices would have on inflation.

Participation in the Fund is NOT a bank deposit or an obligation of, or guaranteed, nor issued, nor insured by Metropolitan Bank & Trust Company or its affiliates or subsidiaries and therefore are not insured or governed by the Philippine Deposit Insurance Corporation (PDIC). Any income and loss arising from market fluctuations and price volatility of the securities held by the fund, even if invested in government securities, is for the account of the investor. As such the fund is not capital protected and may not be suitable for clients seeking preservation of capital. Historical performance when presented is purely for reference purposes and not a guarantee of similar future results. The Declaration of Trust of the Fund is available at the principal office of the Trustee upon request.

Source: metrobank.com.ph